Hsa Personal Finance

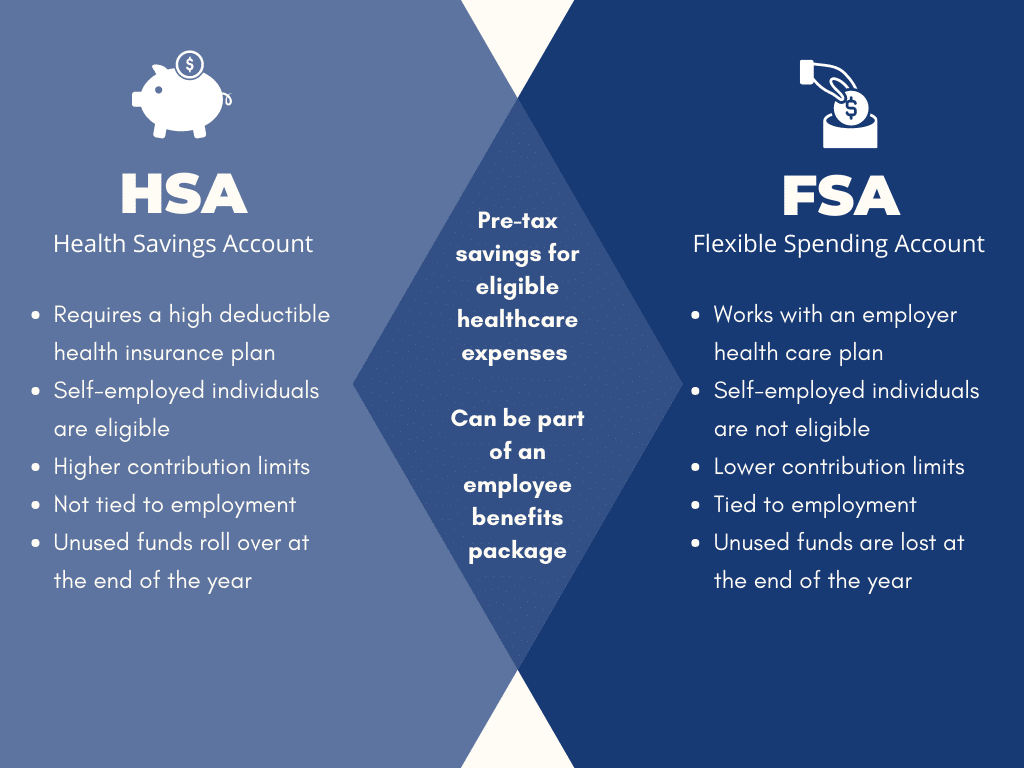

A Health Savings Account (HSA) is a powerful tool for managing healthcare expenses and building long-term savings, offering a triple tax advantage. It's available to individuals with a High-Deductible Health Plan (HDHP), generally defined as having a deductible of at least $1,600 for individuals and $3,200 for families in 2024. An HSA can be a valuable component of your overall personal finance strategy if used effectively.

Triple Tax Advantages

- Tax-Deductible Contributions: Contributions to an HSA are tax-deductible, reducing your taxable income in the year you contribute. This is an "above-the-line" deduction, meaning you don't have to itemize to claim it.

- Tax-Free Growth: The money in your HSA grows tax-free. Similar to a Roth IRA or 401(k), the investment earnings accumulate without being taxed.

- Tax-Free Withdrawals for Qualified Expenses: When you use the money in your HSA to pay for qualified medical expenses, the withdrawals are tax-free. These expenses include doctor visits, prescriptions, vision care, dental care, and more.

HSA as a Savings and Investment Tool

While an HSA is designed for healthcare expenses, it can also function as a potent long-term savings vehicle. Many HSA providers offer investment options, allowing you to invest your HSA funds in stocks, bonds, and mutual funds. By investing your HSA balance, you can potentially grow your savings significantly over time, especially if you don't need to use the funds for immediate healthcare needs.

This "stealth IRA" strategy involves paying for current medical expenses out-of-pocket and letting your HSA grow over time. Then, you can reimburse yourself for those past medical expenses years later, essentially using the HSA as a retirement account.

Eligibility and Contribution Limits

To be eligible for an HSA, you must be enrolled in a qualified HDHP, not be covered by any other health plan (with some exceptions for specific types of coverage like dental or vision), and not be enrolled in Medicare.

Contribution limits are set annually by the IRS. For 2024, the contribution limit is $4,150 for individuals and $8,300 for families. Individuals age 55 and older can contribute an additional $1,000 as a "catch-up" contribution.

Considerations and Potential Drawbacks

While HSAs offer significant benefits, it's essential to consider potential drawbacks:

- High Deductible: The HDHP required to qualify for an HSA can mean higher out-of-pocket costs upfront for healthcare.

- Investment Risk: Investing HSA funds involves market risk. You could lose money if your investments perform poorly.

- Complexity: Understanding HSA rules and regulations can be complex. It's important to research and stay informed.

- Record Keeping: Meticulous record-keeping of medical expenses is essential if you plan to reimburse yourself later for past costs.

In conclusion, an HSA can be a valuable tool for managing healthcare costs and building long-term wealth. By carefully considering your eligibility, contribution strategy, and investment options, you can maximize the benefits of this powerful savings vehicle.

1080×1080 hsa work ultimate hsa guide personal finance club from www.personalfinanceclub.com

1080×1080 hsa work ultimate hsa guide personal finance club from www.personalfinanceclub.com  1080×1080 hsa fsa personal finance club from www.personalfinanceclub.com

1080×1080 hsa fsa personal finance club from www.personalfinanceclub.com  1080×1080 invest max hsa roth ira from www.personalfinanceclub.com

1080×1080 invest max hsa roth ira from www.personalfinanceclub.com  653×1024 hsa optum investments investing personal finance club from community.personalfinanceclub.com

653×1024 hsa optum investments investing personal finance club from community.personalfinanceclub.com  1144×643 hsa hack secret financial planning from financer.com

1144×643 hsa hack secret financial planning from financer.com  800×400 hsa account guide secret wealth building power from barbarafriedbergpersonalfinance.com

800×400 hsa account guide secret wealth building power from barbarafriedbergpersonalfinance.com  3200×1800 hsa kiplinger from www.kiplinger.com

3200×1800 hsa kiplinger from www.kiplinger.com  300×250 health savings account hsa basics from 20somethingfinance.com

300×250 health savings account hsa basics from 20somethingfinance.com  720×720 fsa hsa lose napkin finance from napkinfinance.com

720×720 fsa hsa lose napkin finance from napkinfinance.com  1200×662 hsa forced savings dollar investment club from dollarinvestmentclub.com

1200×662 hsa forced savings dollar investment club from dollarinvestmentclub.com  1920×1080 hsa benefits kiplinger from www.kiplinger.com

1920×1080 hsa benefits kiplinger from www.kiplinger.com  1280×720 hsa explained inflation protection from inflationprotection.org

1280×720 hsa explained inflation protection from inflationprotection.org  800×533 investing hsa contributions youre missing money from money.com

800×533 investing hsa contributions youre missing money from money.com  1280×720 hsa loophole save retirement hsa from mrmoneygeek.com

1280×720 hsa loophole save retirement hsa from mrmoneygeek.com  1280×720 brandpointcontent personal finance from www.brandpointcontent.com

1280×720 brandpointcontent personal finance from www.brandpointcontent.com  1280×854 hsa contributions tax deductible answers essential hsa from credentwealth.com

1280×854 hsa contributions tax deductible answers essential hsa from credentwealth.com  1792×1024 benefits setting hsa health savings account navigate from navigatingfinance.com

1792×1024 benefits setting hsa health savings account navigate from navigatingfinance.com  512×512 invest health savings account hsa maximize returns from www.tffn.net

512×512 invest health savings account hsa maximize returns from www.tffn.net  1024×768 hsa tax benefits alfy louisa from myrtababigael.pages.dev

1024×768 hsa tax benefits alfy louisa from myrtababigael.pages.dev  1024×683 hsa distributions tax savings pay medical expenses from www.myfederalretirement.com

1024×683 hsa distributions tax savings pay medical expenses from www.myfederalretirement.com  640×1024 singapore finance connecting singapores professional services from singaporefinance.org

640×1024 singapore finance connecting singapores professional services from singaporefinance.org  2437×1625 hsa financial designs from www.financialdesignsinc.com

2437×1625 hsa financial designs from www.financialdesignsinc.com  600×343 maximizing hsa account benefits effectively from thealphaman.blog

600×343 maximizing hsa account benefits effectively from thealphaman.blog  320×168 personal finance singaporepdf from www.slideshare.net

320×168 personal finance singaporepdf from www.slideshare.net  600×400 hsa fsa eligible expenses from www.lasikvisioninstitute.com

600×400 hsa fsa eligible expenses from www.lasikvisioninstitute.com  1197×385 singapore hsa enhances legislation facilitate faster access md from www.regdesk.co

1197×385 singapore hsa enhances legislation facilitate faster access md from www.regdesk.co  1200×798 hsa powerful tool personal financial planning process from www.parakletefinancial.com

1200×798 hsa powerful tool personal financial planning process from www.parakletefinancial.com  750×500 hsa primer account save from www.thepennyhoarder.com

750×500 hsa primer account save from www.thepennyhoarder.com  768×1024 reasons hsa save money murphy company cpas from borgidacpas.com

768×1024 reasons hsa save money murphy company cpas from borgidacpas.com