Avg Finance

Here's an HTML-formatted piece on average finance, keeping the word count around 500 and avoiding unnecessary tags:

Average finance encapsulates the financial realities experienced by the typical household. It's a broad concept encompassing income, expenses, savings, debt, and investment strategies pursued by the majority. Understanding average finance provides a benchmark for individuals to assess their own financial standing and identify areas for improvement.

Income, often the primary driver of financial well-being, varies significantly based on factors like education, occupation, location, and experience. Median household income provides a useful average, though it's important to note regional disparities and the impact of cost of living. Beyond wages, income may also include returns from investments, rental properties, or government benefits.

Expenses represent the outflow of money to cover essential needs and discretionary wants. Housing, transportation, food, and healthcare constitute significant portions of the average household budget. Discretionary spending includes entertainment, travel, and non-essential goods. Tracking expenses is crucial for understanding where money is going and identifying potential areas for cost reduction. Budgeting, whether through spreadsheets or dedicated apps, helps manage spending and align it with financial goals.

Savings play a vital role in financial security, providing a buffer against unexpected expenses and funding future goals like retirement or homeownership. The average savings rate, representing the percentage of income saved, varies widely across demographics. Building an emergency fund containing 3-6 months' worth of living expenses is a fundamental principle of sound personal finance. Retirement savings, often through employer-sponsored plans like 401(k)s or individual retirement accounts (IRAs), are essential for long-term financial stability.

Debt is a common feature of average finance, often incurred for major purchases like homes, cars, or education. Managing debt responsibly is crucial to avoid financial strain. High-interest debt, such as credit card balances, should be prioritized for repayment. Understanding interest rates, loan terms, and repayment strategies is essential for navigating debt effectively. Avoiding unnecessary debt and minimizing borrowing costs are key principles for improving financial health.

Investments represent a pathway to growing wealth over time. The average investment portfolio often includes a mix of stocks, bonds, and mutual funds. Diversification, spreading investments across different asset classes, helps manage risk. Investing requires understanding risk tolerance, investment horizons, and market dynamics. Seeking professional financial advice can be beneficial for developing a personalized investment strategy.

Ultimately, average finance serves as a valuable reference point. By understanding the financial realities of the typical household, individuals can gain insights into their own financial situation, identify areas for improvement, and make informed decisions to achieve their financial goals. Continuous learning and adaptation are key to navigating the ever-changing landscape of personal finance and achieving long-term financial well-being.

3420×1768 avg performance update from now.avg.com

3420×1768 avg performance update from now.avg.com  1920×1000 avg official blog security news tips avg blogs from now.avg.com

1920×1000 avg official blog security news tips avg blogs from now.avg.com  1200×997 avg from avgbags.com

1200×997 avg from avgbags.com  1000×1400 resources newsroom avg technologies from www.avg.com

1000×1400 resources newsroom avg technologies from www.avg.com  1296×981 avg store explore products prices buy avg from www.avg.com

1296×981 avg store explore products prices buy avg from www.avg.com  900×600 avg media case study victory management group from www.vmg1.com

900×600 avg media case study victory management group from www.vmg1.com  743×398 av finance financial services individuals businesses av finance from av-finance.co.uk

743×398 av finance financial services individuals businesses av finance from av-finance.co.uk  3494×1268 av finance financial services individuals businesses av from commercial.av-finance.co.uk

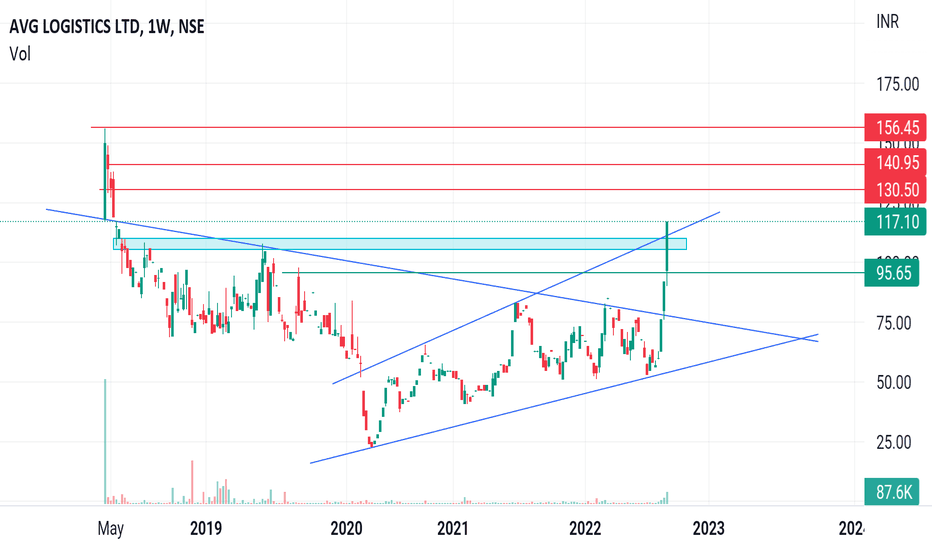

3494×1268 av finance financial services individuals businesses av from commercial.av-finance.co.uk  932×550 avg stock price chart nseavg tradingview india from in.tradingview.com

932×550 avg stock price chart nseavg tradingview india from in.tradingview.com  1200×900 avg meaning fluentslang from fluentslang.com

1200×900 avg meaning fluentslang from fluentslang.com  466×275 avg stock price chart asxavg tradingview from www.tradingview.com

466×275 avg stock price chart asxavg tradingview from www.tradingview.com  600×600 avg technologies affiliate program affiliate monkey from theaffiliatemonkey.com

600×600 avg technologies affiliate program affiliate monkey from theaffiliatemonkey.com  1024×1024 avg logo vector logo avg brand eps ai png cdr from www.logotypes101.com

1024×1024 avg logo vector logo avg brand eps ai png cdr from www.logotypes101.com  768×432 dri avg technologies avg payment explained from wendywaldman.com

768×432 dri avg technologies avg payment explained from wendywaldman.com  850×200 avg regular softvire uk from uk.softvire.net

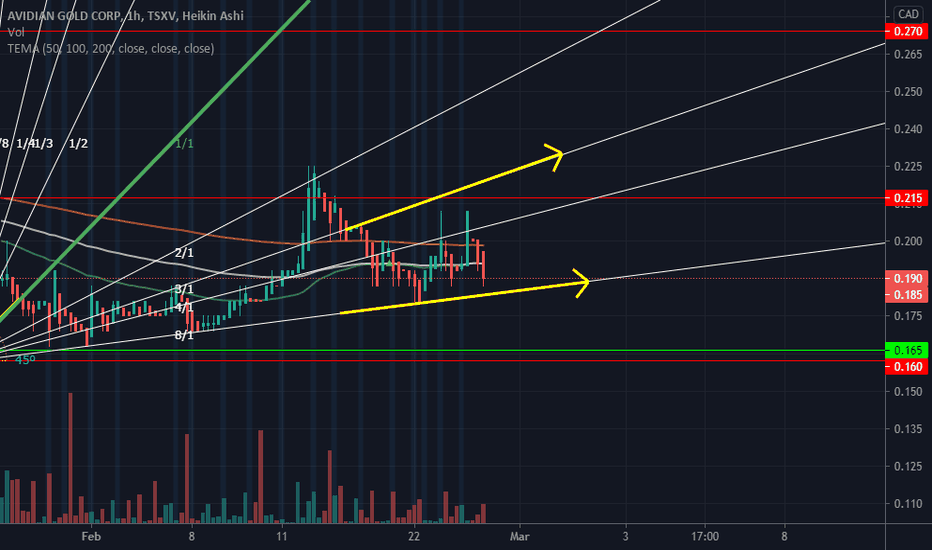

850×200 avg regular softvire uk from uk.softvire.net  932×550 avg stock price chart tsxvavg tradingview from www.tradingview.com

932×550 avg stock price chart tsxvavg tradingview from www.tradingview.com  474×238 avg business single edition year subscription midwest from midwestmicro.us

474×238 avg business single edition year subscription midwest from midwestmicro.us  600×733 development finance cvg finance from www.cvgfinance.com.au

600×733 development finance cvg finance from www.cvgfinance.com.au  600×799 investment finance cvg finance from www.cvgfinance.com.au

600×799 investment finance cvg finance from www.cvgfinance.com.au  955×504 avg logistics stock untested worth good valuepickr forum from forum.valuepickr.com

955×504 avg logistics stock untested worth good valuepickr forum from forum.valuepickr.com  1300×942 singaporean finance stock photo alamy from www.alamy.com

1300×942 singaporean finance stock photo alamy from www.alamy.com  1000×750 hedge funds avg technologies nv avg insider monkey from www.insidermonkey.com

1000×750 hedge funds avg technologies nv avg insider monkey from www.insidermonkey.com  620×234 security review avg internet security digital citizen from www.digitalcitizen.life

620×234 security review avg internet security digital citizen from www.digitalcitizen.life